What Is the AI Factor?

What is the AI Factor?

What Is the AI Factor?

The AI Factor on Portfolio123.com represents an innovative integration of artificial intelligence into quantitative investment strategies without the need to write any code.

By combining AI with fundamental and technical data, the AI Factor bridges the gap between traditional factor-based investing and AI based data analysis.

The AI Factor employs advanced machine learning techniques applied to a vast database of historical financial and market data. It systematically evaluates and scores stocks based on their likelihood of outperforming or underperforming a selected benchmark.

Unlike conventional factors such as value, momentum, or quality, the AI Factor dynamically adapts to changing market conditions and captures nonlinear relationships in the data that traditional methods may overlook.

Key Benefits

Effortless Integration: Seamlessly incorporated into the Portfolio123 platform, ensuring a smooth user experience.

User-Friendly Design: No coding skills are required, making it accessible to all investors.

Superior Predictive Power: Provides enhanced predictive performance through sophisticated machine learning models.

Clear Insights: Transparency is achieved via factor importance-metrics, helping users understand the key drivers of the model.

Robust Testing Framework: Rigorous out-of-sample testing validates the reliability of predictions.

Customizable Machine Learning Models: Offers flexibility for users to fine-tune hyperparameters and adapt strategies to their needs.

Comprehensive Data Analysis: Analyzes massive datasets with hundreds of features (factors), capturing nuanced relationships that traditional models may miss or take extensive time to test.

Key Features

Machine Learning Models: Utilizes supervised learning techniques to identify patterns in financial data. These models are trained on years of historical stock performance, along with fundamental, technical, and macroeconomic variables.

Dynamic Scoring System: Assigns scores to securities based on their likelihood of future outperformance, with periodic retraining to incorporate new data and adapt to evolving market dynamics.

Integration: Allows users to incorporate the AI Factor into custom screens, ranking systems, and portfolio strategies seamlessly.

Transparency: Despite the inherent complexity of AI models, Portfolio123 provides insights into how the factor interacts with other variables, enabling users to evaluate its predictive power and limitations.

Use Cases

Long only or long-short portfolios: Combine AI Factor into your existing quantitative or technical strategies or create new strategies based solely on the AI's predictions.

Stock Screening: Filters out stocks with low potential while prioritizing those with higher scores.

Factor Blending: Complements traditional factors such as value and growth, creating more robust multi-factor strategies.

Enhance existing strategies: AI Factor as a filter to identify potential underperformers, helping to reduce portfolio risk and enhance Sharpe ratios.

Sector Rotation: Dynamically adjusts to macroeconomic and sector-specific changes, making it a powerful tool for sector allocation decisions.

Conclusion

The AI Factor on Portfolio123.com represents a significant leap forward in quantitative investing. By combining machine learning with traditional factor analysis, it equips investors with a cutting-edge tool to navigate today’s complex markets. Thoughtful utilization of the AI Factor can enhance decision-making and deliver improved investment outcomes.

Appendix

- Example Strategy

Example Strategy

- Target: 6 Month relative strength to S&P 500

- Dataset: 2003-01-01 to 2024-07-13 (21.5 years)

- Universe: S&P 500

- Features (Factors): 365

- Normalization / Scaling: Rank

- Validation Method: Basic Holdout

- Validation Training Period: 17.2 years

- Gap: 24 Weeks

- Portfolio Holdout: 46 Months

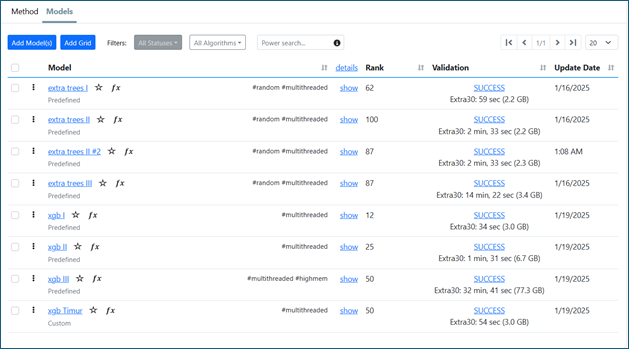

Applied Machine Learning Models (Validation):

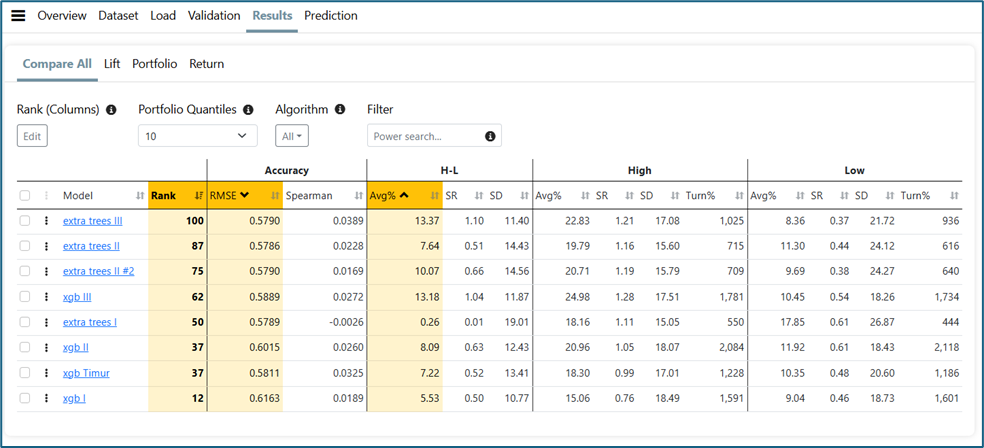

Validation Results: Compare ML Models

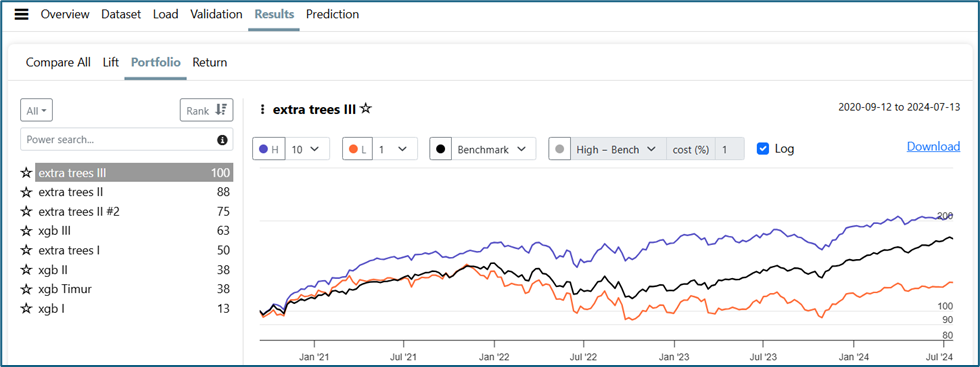

Validation Results: Portfolio

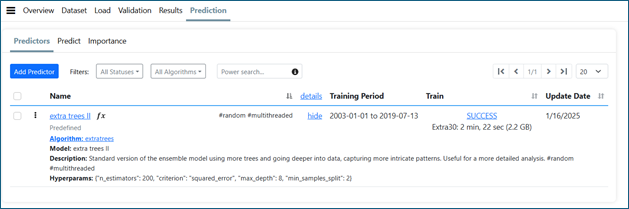

Predictor: Training

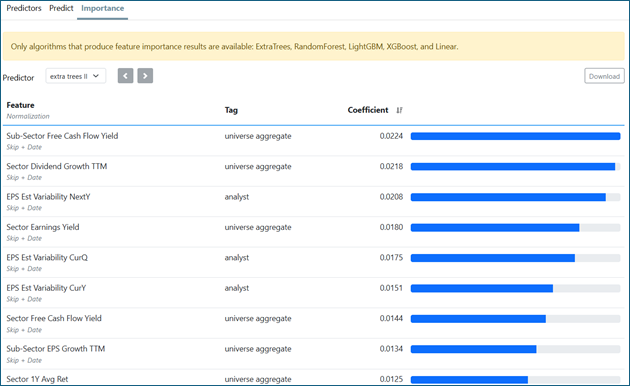

Predictor: Feature Importance

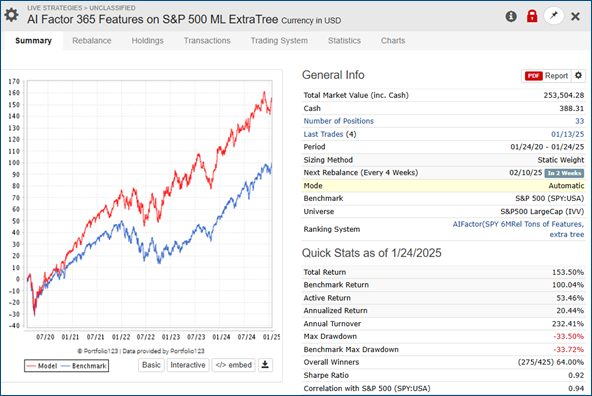

Out of Sample Test Portfolio Strategy with Predictor 100% weighting in Ranking System. S&P 500 Universe. Static weight, weekly rebalance, 33 Stocks.

Did this answer your question?